Managing money in today’s economy isn’t just about earning more — it’s about making smarter decisions with what you already have. With rising living costs, shifting interest rates, and evolving investment options, Americans need a strategy that works in real life — not just in theory.

Whether you’re in your 20s building your foundation or in your 50s accelerating retirement savings, this guide breaks down practical financial strategies for U.S. households in 2026.

1️⃣ Build a Strong Financial Foundation

Before diving into investing or real estate, start with the basics.

✔ Create a Zero-Based Budget

Every dollar should have a purpose:

- Housing

- Utilities

- Insurance

- Debt payments

- Savings

- Investments

- Lifestyle spending

Apps offered by institutions like Bank of America and Chase help automate tracking and categorize expenses.

Goal: Avoid lifestyle creep and identify savings opportunities each month.

2️⃣ Eliminate High-Interest Debt First

Credit card interest rates in the U.S. often exceed 20%. That’s higher than most investment returns.

Two Popular Payoff Strategies:

- Snowball Method – Pay off smallest balances first.

- Avalanche Method – Focus on highest interest rates first.

If debt is overwhelming, consider balance transfer cards or consolidation loans from trusted providers like Discover.

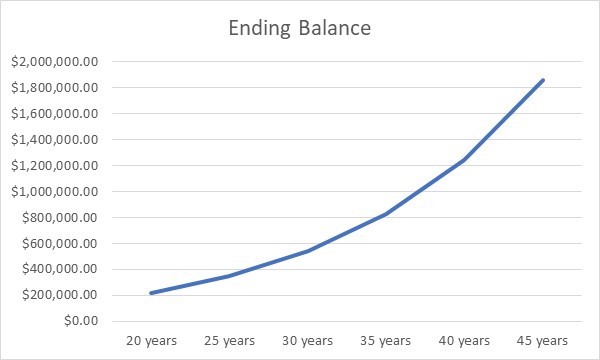

3️⃣ Make Retirement Accounts Work for You

4

The U.S. tax code strongly encourages retirement investing.

🏦 401(k)

If your employer matches contributions, contribute at least enough to get the full match — it’s essentially a guaranteed return.

Common 401(k) administrators include:

- Fidelity Investments

- Vanguard

- T. Rowe Price

🏛 Roth IRA

Ideal if you expect higher income later. You pay taxes now, but withdrawals in retirement are tax-free.

4️⃣ Diversify Investments Beyond Just Stocks

While the Dow Jones Industrial Average and S&P 500 dominate headlines, diversification reduces risk.

Consider allocating across:

- U.S. large-cap stocks

- International stocks

- Bonds

- Real estate (REITs)

- Treasury securities

Low-cost ETFs from Charles Schwab or Vanguard make diversification accessible to beginners.

5️⃣ Understand Today’s Housing Market

4

Mortgage rates fluctuate based on Federal Reserve policies and economic conditions.

High-growth states such as Florida, North Carolina, and Arizona continue to attract buyers due to job growth and population shifts.

Before buying:

- Maintain a strong credit score (700+ preferred)

- Keep debt-to-income ratio below 36%

- Save at least 10–20% for down payment (if possible)

6️⃣ Optimize Taxes Like the Wealthy Do

Smart tax planning isn’t just for high earners.

Here are powerful tools:

✔ Health Savings Accounts (HSA)

✔ 529 College Savings Plans

✔ Tax-loss harvesting

✔ Long-term capital gains strategy

✔ Backdoor Roth IRA (for high-income earners)

Consider consulting a CPA for advanced strategies.

7️⃣ Build Multiple Income Streams

In today’s economy, relying on one paycheck is risky.

Popular U.S. side income options:

- Freelancing

- Rental income

- Dividend investing

- Online businesses

- High-yield savings and CDs

Platforms from companies like SoFi offer integrated tools for investing, banking, and automated savings.

8️⃣ Protect Your Financial Future

Financial security isn’t only about growth — it’s about risk management.

Essential protections:

- Term life insurance

- Disability insurance

- Emergency fund (6 months of expenses)

- Estate plan (Will & Trust)

Without protection, one unexpected event can undo years of progress.

Final Thoughts: The 2026 American Money Blueprint

Wealth building in the United States still follows a proven formula:

- Control spending

- Eliminate toxic debt

- Max retirement accounts

- Invest consistently

- Diversify assets

- Protect your downside

Consistency beats intensity every time.