Introduction

With inflation pressures, fluctuating interest rates, and economic uncertainty, Americans are thinking more seriously about how to protect and grow their money. Whether you’re earning $50,000 or $250,000 a year, the rules of smart financial management remain the same — spend intentionally, invest strategically, and prepare for the unexpected.

In this guide, we’ll break down practical, realistic strategies for budgeting, saving, investing, retirement planning, and reducing taxes — specifically designed for U.S. households in 2026.

1️⃣ Master Your Cash Flow Before Investing

Before you invest in stocks or real estate, you must control your monthly cash flow.

The 50/30/20 Rule (Updated for Today’s Economy)

- 50% Needs – Housing, utilities, groceries, insurance

- 30% Wants – Dining out, travel, entertainment

- 20% Savings & Investing – Retirement, brokerage accounts, emergency fund

In high-cost states like California or New York, you may need a 60/20/20 variation due to rent prices.

Pro Tip:

Automate transfers to savings immediately after payday. What you don’t see, you won’t spend.

2️⃣ Build a Fully Funded Emergency Fund

Americans faced major lessons during COVID-19 and recent layoffs in tech and finance sectors.

Aim for:

- 3–6 months of expenses (stable job)

- 6–9 months (self-employed or commission-based income)

Store this money in a high-yield savings account (HYSA), not a traditional savings account.

Banks like:

- Ally Bank

- Capital One

- SoFi

…often offer competitive APYs compared to brick-and-mortar banks.

3️⃣ Maximize Retirement Accounts (Tax Advantages Matter)

The U.S. tax system rewards retirement investing. Take advantage of it.

🏢 401(k) – Employer-Sponsored Plan

If your employer offers a match, contribute at least enough to get the full match. It’s free money.

Example:

If your employer matches 4%, and you earn $80,000:

You’re leaving $3,200/year on the table if you don’t contribute.

Major providers include:

- Fidelity Investments

- Vanguard

- Charles Schwab

🏦 Roth IRA vs Traditional IRA

- Roth IRA → Pay taxes now, withdraw tax-free later

- Traditional IRA → Tax deduction now, pay taxes later

If you expect higher income in retirement, Roth is often powerful.

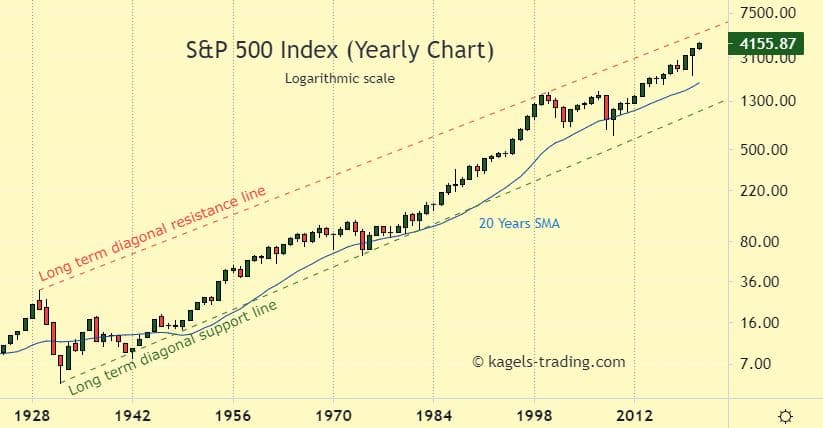

4️⃣ Invest Smartly in the U.S. Stock Market

4

Historically, the U.S. stock market has averaged about 8–10% annual returns long-term.

Instead of picking individual stocks, many Americans invest in:

- Index funds tracking the S&P 500

- Total market funds

- ETFs like those offered by Vanguard

Why Index Funds Win:

- Low fees

- Broad diversification

- Passive strategy reduces emotional trading

5️⃣ Real Estate: Still a Strong Wealth Builder?

4

Despite higher mortgage rates, real estate remains a popular wealth-building tool in states like Texas and Florida due to population growth.

Options include:

- Primary home ownership

- Rental properties

- REITs (Real Estate Investment Trusts)

Be cautious:

- Property taxes vary by state

- Insurance premiums are rising in coastal areas

- Cash flow matters more than appreciation

6️⃣ Reduce Taxes Legally (Most Americans Miss This)

Here are often-overlooked strategies:

✔ Max out HSA (Health Savings Account)

✔ Use 529 plans for education savings

✔ Harvest tax losses in brokerage accounts

✔ Contribute to pre-tax retirement plans

The IRS rewards long-term investing and retirement planning — take advantage of it.

7️⃣ Protect Your Wealth

Wealth building isn’t just about growth — it’s also about protection.

Essential protections:

- Term life insurance (if you have dependents)

- Disability insurance

- Umbrella liability insurance

- Estate planning documents (Will, Power of Attorney)

8️⃣ Avoid These Common American Money Mistakes

🚫 Carrying high-interest credit card debt

🚫 Trying to time the market

🚫 Ignoring inflation

🚫 Not negotiating salary

🚫 Lifestyle inflation after promotions

Final Thoughts: The American Wealth Formula

Building wealth in the U.S. isn’t about luck. It’s about consistency:

- Spend less than you earn

- Automate investments

- Maximize tax-advantaged accounts

- Invest long-term

- Protect what you build

The earlier you start, the more compounding works in your favor.